Kirana Transformation in India

- 1. KIRANA TRANSFORMATION ININDIA Measuring the impact of kirana transformation An approach to promote retail sector modernization in India April 2020

- 2. Changing Retail Landscape Research a. Methodology b. Findings c. Benefits of Transformation Transformation Process Challenges Role of Stakeholders Recommendations Appendix Contents Importance of Traditional Trade in India1 2 4 5 6 7 8 2 3

- 3. 3 IMPORTANCE OFTRADITIONAL TRADE IN INDIA

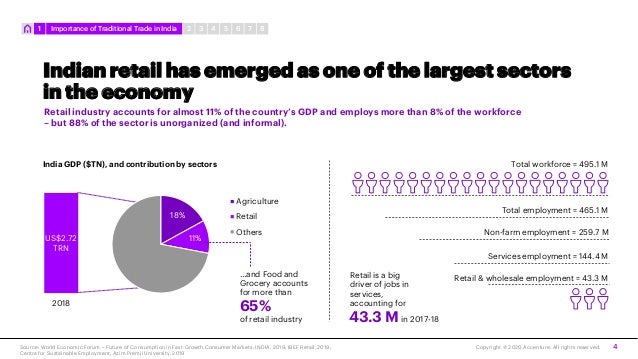

- 4. Retail industry accounts for almost 11% of the country’s GDP and employs more than 8% of the workforce – but 88% of the sector is unorganized (and informal). US$2.72 TRN 2018 India GDP ($TN), and contribution by sectors 18% 11% Agriculture Retail Others Copyright © 2020 Accenture. All rights reserved.Source: World Economic Forum – Future of Consumption in Fast-Growth Consumer Markets: INDIA, 2019; IBEF Retail, 2019; Centre for Sustainable Employment, Azim Premji University, 2019 4 Indian retail has emerged as one of the largest sectors in the economy Total employment = 465.1 M Non-farm employment = 259.7 M Services employment = 144.4 M Retail & wholesale employment = 43.3 M Total workforce = 495.1 M 43.3 M Retail is a big driver of jobs in services, accounting for in 2017-18 65% …and Food and Grocery accounts for more than of retail industry 87654321 Importance of Traditional Trade in India

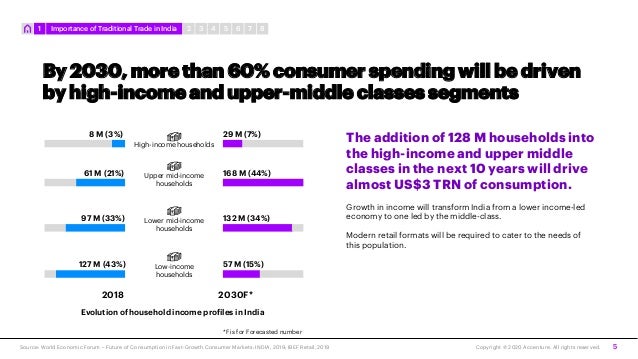

- 5. Copyright © 2020 Accenture. All rights reserved.Source: World Economic Forum – Future of Consumption in Fast-Growth Consumer Markets: INDIA, 2019; IBEF Retail, 2019 5 By 2030, more than 60% consumer spending will be driven by high-income and upper-middle classes segments Evolution of household income profiles in India Low-income households Lower mid-income households Upper mid-income households High-income households 2018 2030F* 61 M (21%) 168 M (44%) 97 M (33%) 132 M (34%) 127 M (43%) 57 M (15%) 8 M (3%) 29 M (7%) The addition of 128 M households into the high-income and upper middle classes in the next 10 years will drive almost US$3 TRN of consumption. Growth in income will transform India from a lower income-led economy to one led by the middle-class. Modern retail formats will be required to cater to the needs of this population. 87654321 Importance of Traditional Trade in India *F is for Forecasted number

- 6. 6 CHANGING RETAIL LANDSCAPE

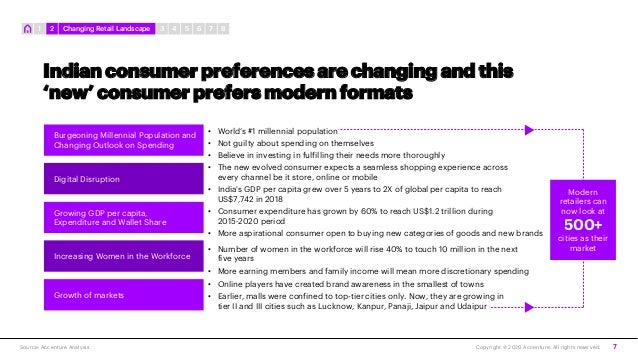

- 7. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 7 Indian consumer preferences are changing and this ‘new’ consumer prefers modern formats Burgeoning Millennial Population and Changing Outlook on Spending Digital Disruption Growing GDP per capita, Expenditure and Wallet Share Increasing Women in the Workforce Growth of markets • World’s #1 millennial population • Not guilty about spending on themselves • Believe in investing in fulfilling their needs more thoroughly • The new evolved consumer expects a seamless shopping experience across every channel be it store, online or mobile • India's GDP per capita grew over 5 years to 2X of global per capita to reach US$7,742 in 2018 • Consumer expenditure has grown by 60% to reach US$1.2 trillion during 2015-2020 period • More aspirational consumer open to buying new categories of goods and new brands • Number of women in the workforce will rise 40% to touch 10 million in the next five years • More earning members and family income will mean more discretionary spending • Online players have created brand awareness in the smallest of towns • Earlier, malls were confined to top-tier cities only. Now, they are growing in tier II and III cities such as Lucknow, Kanpur, Panaji, Jaipur and Udaipur Modern retailers can now look at 500+ cities as their market 87654321 Changing Retail Landscape

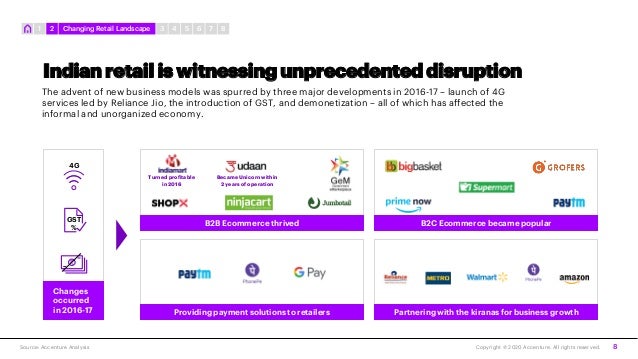

- 8. The advent of new business models was spurred by three major developments in 2016-17 – launch of 4G services led by Reliance Jio, the introduction of GST, and demonetization – all of which has affected the informal and unorganized economy. B2B Ecommerce thrived Providing payment solutions to retailers B2C Ecommerce became popular Partnering with the kiranas for business growth Turned profitable in 2016 Became Unicorn within 2 years of operation Changes occurred in 2016-17 Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 8 Indian retail is witnessing unprecedented disruption GST % 4G 87654321 Changing Retail Landscape

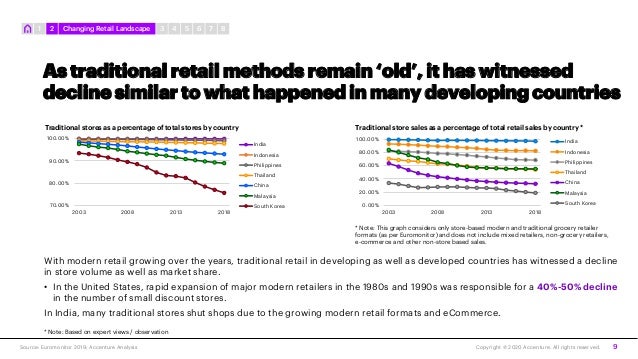

- 9. 70.00% 80.00% 90.00% 100.00% 2003 2008 2013 2018 Traditional stores as a percentage of total stores by country India Indonesia Philippines Thailand China Malaysia South Korea With modern retail growing over the years, traditional retail in developing as well as developed countries has witnessed a decline in store volume as well as market share. • In the United States, rapid expansion of major modern retailers in the 1980s and 1990s was responsible for a 40%-50% decline in the number of small discount stores. In India, many traditional stores shut shops due to the growing modern retail formats and eCommerce. * Note: This graph considers only store-based modern and traditional grocery retailer formats (as per Euromonitor) and does not include mixed retailers, non-grocery retailers, e-commerce and other non-store based sales. Copyright © 2020 Accenture. All rights reserved.Source: Euromonitor 2019; Accenture Analysis 9 As traditional retail methods remain ‘old’, it has witnessed decline similar to what happened in many developing countries 0.00% 20.00% 40.00% 60.00% 80.00% 100.00% 2003 2008 2013 2018 India Indonesia Philippines Thailand China Malaysia South Korea Traditional store sales as a percentage of total retail sales by country * 87654321 Changing Retail Landscape * Note: Based on expert views / observation

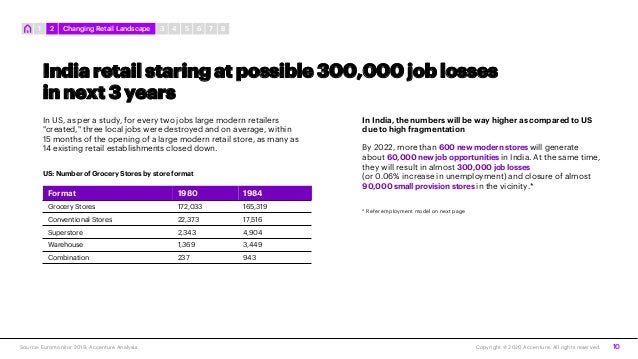

- 10. In US, as per a study, for every two jobs large modern retailers "created," three local jobs were destroyed and on average, within 15 months of the opening of a large modern retail store, as many as 14 existing retail establishments closed down. US: Number of Grocery Stores by store format Format 1980 1984 Grocery Stores 172,033 165,319 Conventional Stores 22,373 17,516 Superstore 2,343 4,904 Warehouse 1,369 3,449 Combination 237 943 In India, the numbers will be way higher as compared to US due to high fragmentation By 2022, more than 600 new modern stores will generate about 60,000 new job opportunities in India. At the same time, they will result in almost 300,000 job losses (or 0.06% increase in unemployment) and closure of almost 90,000 small provision stores in the vicinity.* * Refer employment model on next page Copyright © 2020 Accenture. All rights reserved.Source: Euromonitor 2019; Accenture Analysis 10 India retail staring at possible 300,000 job losses in next 3 years 87654321 Changing Retail Landscape

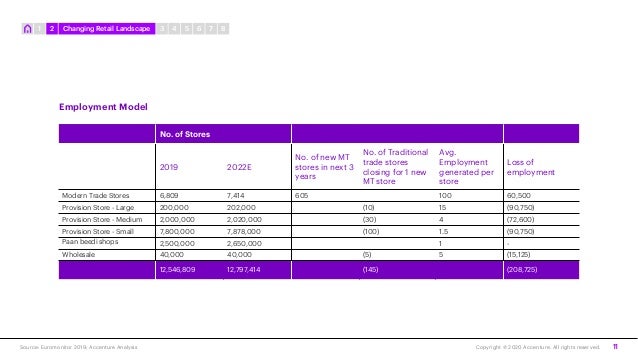

- 11. Copyright © 2020 Accenture. All rights reserved.Source: Euromonitor 2019; Accenture Analysis 11 87654321 Changing Retail Landscape No. of Stores 2019 2022E No. of new MT stores in next 3 years No. of Traditional trade stores closing for 1 new MT store Avg. Employment generated per store Loss of employment Modern Trade Stores 6,809 7,414 605 100 60,500 Provision Store - Large 200,000 202,000 (10) 15 (90,750) Provision Store - Medium 2,000,000 2,020,000 (30) 4 (72,600) Provision Store - Small 7,800,000 7,878,000 (100) 1.5 (90,750) Paan beedi shops 2,500,000 2,650,000 1 - Wholesale 40,000 40,000 (5) 5 (15,125) 12,546,809 12,797,414 (145) (208,725) Employment Model

- 12. Though India falls in the third wave of retail modernization in developing economies, retail revolution has barely got underway due to a protectionist approach aimed at insulating local players and largely against foreign investments. To revolutionize retail sustainably, it is critical to assist local firms (retailers and suppliers) to adapt to modern retailing so they can benefit from productivity gains. The next 10-12 years will be the defining years for Indian retail as – Copyright © 2020 Accenture. All rights reserved.Source: Making retail modernization In developing countries inclusive, GIZ, Germany, 2016; Accenture Analysis 12 Most of the Indian retail sector has barely seen modernization in last 20 years 1st Wave: Early 1990s 2nd Wave: Mid to late 1990s 3rd Wave: Early 2000s 4th Wave: Late 2000s South America, East Asia (outside China and Japan), parts of Southeast Asia (e.g. the Philippines and Thailand), North- Central Europe and South Africa Mexico and parts of Central America, Indonesia, South- Central Europe and South Africa China, Eastern Europe, Russia, other parts of Central America and Southeast Asia, and India South Asia (outside India), sub-Saharan Africa, poorer countries in Southeast Asia (e.g. Cambodia), Bolivia Retail transformation waves in emerging markets (spatial expansion outside North America and Western Europe) 87654321 Changing Retail Landscape • The market will mature and organized retail will penetrate deeper into smaller cities and towns • More international brands and retailers across categories and formats will aggressively enter and grow the Indian business, plus India will become the key growth market for the ones already present • Technology will shape the future path of consumption and new markets or channels could emerge

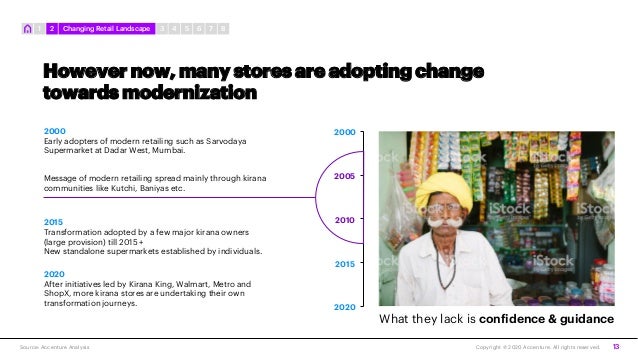

- 13. 2000 2005 2010 2015 2020 Early adopters of modern retailing such as Sarvodaya Supermarket at Dadar West, Mumbai. Message of modern retailing spread mainly through kirana communities like Kutchi, Baniyas etc. Transformation adopted by a few major kirana owners (large provision) till 2015 + New standalone supermarkets established by individuals. After initiatives led by Kirana King, Walmart, Metro and ShopX, more kirana stores are undertaking their own transformation journeys. What they lack is confidence & guidance Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 13 However now, many stores are adopting change towards modernization 2000 2015 2020 87654321 Changing Retail Landscape

- 14. 14 RESEARCH

- 15. DOES KIRANA TRANSFORMATION WORK? OUR RESEARCH FINDS OUT 15 * Note: Kirana Transformation comprises of below 3 parameters of the store – • Self-service format with check-out counters and shopping trollies / baskets in place • Mode of accepting digital payments – cards and wallets • Use of Technology for computerized billing, inventory management etc. • Use of modern retail principles for store management e.g. buying and selling products Copyright © 2020 Accenture. All rights reserved. 87654321 Research

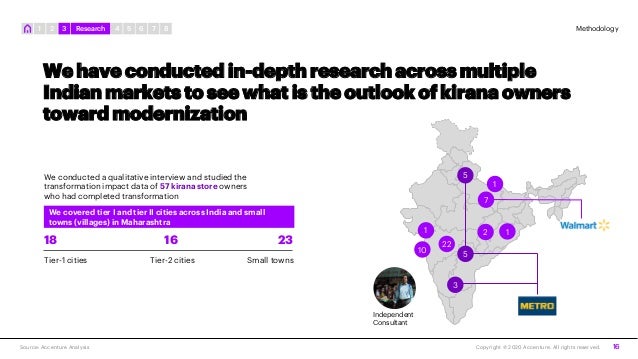

- 16. We have conducted in-depth research across multiple Indian markets to see what is the outlook of kirana owners toward modernization Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 16 We conducted a qualitative interview and studied the transformation impact data of 57 kirana store owners who had completed transformation 18 16 23 Tier-1 cities Tier-2 cities Small towns We covered tier I and tier II cities across India and small towns (villages) in Maharashtra 10 22 7 5 3 5 121 1 Independent Consultant Methodology87654321 Research

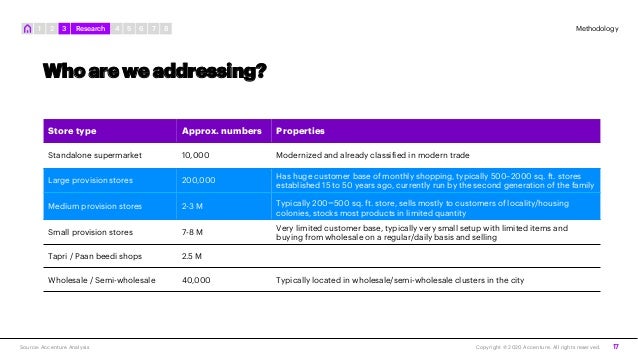

- 17. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 17 Who are we addressing? Store type Approx. numbers Properties Standalone supermarket 10,000 Modernized and already classified in modern trade Large provision stores 200,000 Has huge customer base of monthly shopping, typically 500–2000 sq. ft. stores established 15 to 50 years ago, currently run by the second generation of the family Medium provision stores 2-3 M Typically 200–500 sq. ft. store, sells mostly to customers of locality/housing colonies, stocks most products in limited quantity Small provision stores 7-8 M Very limited customer base, typically very small setup with limited items and buying from wholesale on a regular/daily basis and selling Tapri / Paan beedi shops 2.5 M Wholesale / Semi-wholesale 40,000 Typically located in wholesale/semi-wholesale clusters in the city Methodology87654321 Research

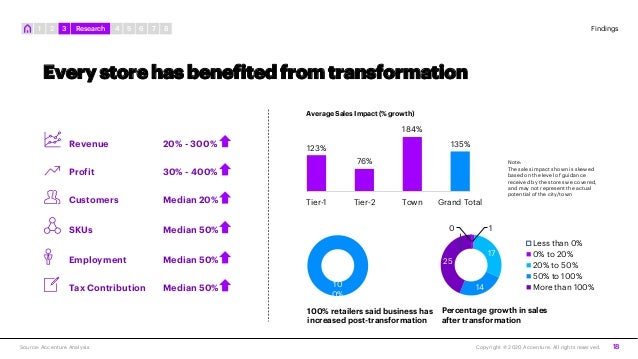

- 18. 0 1 17 14 25 Less than 0% 0% to 20% 20% to 50% 50% to 100% More than 100% Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 18 Every store has benefited from transformation Revenue Profit Tax Contribution Employment 20% - 300% 30% - 400% Median 50% Median 50% SKUs Customers Median 20% Median 50% 123% 76% 184% 135% Tier-1 Tier-2 Town Grand Total Average Sales Impact (% growth) Note: The sales impact shown is skewed based on the level of guidance received by the stores we covered, and may not represent the actual potential of the city/town 10 0% 100% retailers said business has increased post-transformation Percentage growth in sales after transformation Findings87654321 Research

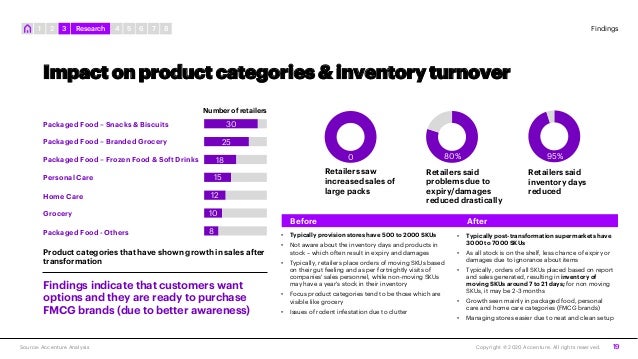

- 19. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 19 Impact on product categories & inventory turnover 30 25 18 15 12 10 8 Product categories that have shown growth in sales after transformation Number of retailers Findings indicate that customers want options and they are ready to purchase FMCG brands (due to better awareness) Packaged Food – Snacks & Biscuits Packaged Food – Branded Grocery Packaged Food – Frozen Food & Soft Drinks Personal Care Home Care Grocery Packaged Food - Others 10 0 % Retailers saw increased sales of large packs 80% Retailers said problems due to expiry/damages reduced drastically 95% Retailers said inventory days reduced • Typically provision stores have 500 to 2000 SKUs • Not aware about the inventory days and products in stock – which often result in expiry and damages • Typically, retailers place orders of moving SKUs based on their gut feeling and as per fortnightly visits of companies' sales personnel, while non-moving SKUs may have a year's stock in their inventory • Focus product categories tend to be those which are visible like grocery • Issues of rodent infestation due to clutter • Typically post-transformation supermarkets have 3000 to 7000 SKUs • As all stock is on the shelf, less chance of expiry or damages due to ignorance about items • Typically, orders of all SKUs placed based on report and sales generated, resulting in inventory of moving SKUs around 7 to 21 days; for non moving SKUs, it may be 2-3 months • Growth seen mainly in packaged food, personal care and home care categories (FMCG brands) • Managing stores easier due to neat and clean setup Before After Findings87654321 Research

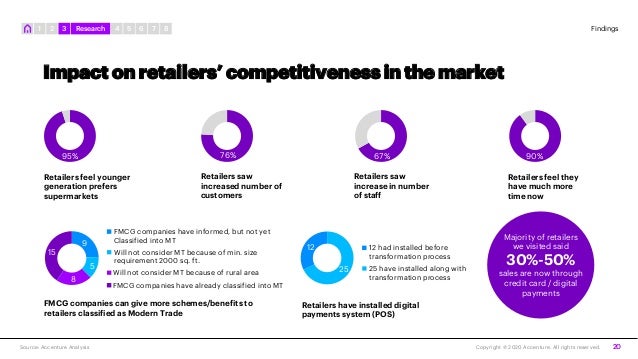

- 20. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 20 Impact on retailers’ competitiveness in the market 95% Retailers feel younger generation prefers supermarkets 76% Retailers saw increased number of customers 67% Retailers saw increase in number of staff 90% Retailers feel they have much more time now 9 5 8 15 FMCG companies can give more schemes/benefits to retailers classified as Modern Trade 25 12 Retailers have installed digital payments system (POS) Majority of retailers we visited said 30%-50% sales are now through credit card / digital payments Findings FMCG companies have informed, but not yet Classified into MT Will not consider MT because of min. size requirement 2000 sq. ft. Will not consider MT because of rural area FMCG companies have already classified into MT 87654321 Research 12 had installed before transformation process 25 have installed along with transformation process

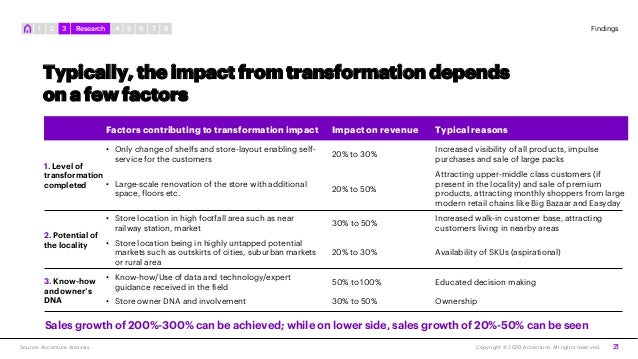

- 21. Factors contributing to transformation impact Impact on revenue Typical reasons • Only change of shelfs and store-layout enabling self- service for the customers 20% to 30% Increased visibility of all products, impulse purchases and sale of large packs • Large-scale renovation of the store with additional space, floors etc. 20% to 50% Attracting upper-middle class customers (if present in the locality) and sale of premium products, attracting monthly shoppers from large modern retail chains like Big Bazaar and Easyday • Store location in high footfall area such as near railway station, market 30% to 50% Increased walk-in customer base, attracting customers living in nearby areas • Store location being in highly untapped potential markets such as outskirts of cities, suburban markets or rural area 20% to 30% Availability of SKUs (aspirational) • Know-how/Use of data and technology/expert guidance received in the field 50% to 100% Educated decision making • Store owner DNA and involvement 30% to 50% Ownership Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 21 Typically, the impact from transformation depends on a few factors 2. Potential of the locality 3. Know-how and owner’s DNA 1. Level of transformation completed Findings87654321 Research Sales growth of 200%-300% can be achieved; while on lower side, sales growth of 20%-50% can be seen

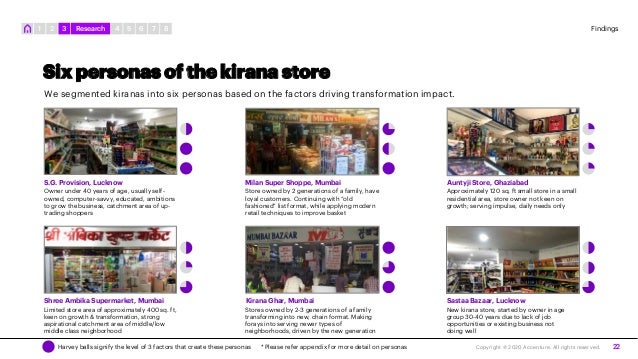

- 22. Copyright © 2020 Accenture. All rights reserved. 22 Six personas of the kirana store Harvey balls signify the level of 3 factors that create these personas * Please refer appendix for more detail on personas We segmented kiranas into six personas based on the factors driving transformation impact. S.G. Provision, Lucknow Owner under 40 years of age, usually self- owned, computer-savvy, educated, ambitions to grow the business, catchment area of up- trading shoppers Store owned by 2 generations of a family, have loyal customers. Continuing with “old fashioned” list format, while applying modern retail techniques to improve basket Approximately 120 sq. ft small store in a small residential area, store owner not keen on growth; serving impulse, daily needs only Milan Super Shoppe, Mumbai Auntyji Store, Ghaziabad Shree Ambika Supermarket, Mumbai Limited store area of approximately 400 sq. ft, keen on growth & transformation, strong aspirational catchment area of middle/low middle class neighborhood Stores owned by 2-3 generations of a family transforming into new, chain format. Making forays into serving newer types of neighborhoods, driven by the new generation New kirana store, started by owner in age group 30-40 years due to lack of job opportunities or existing business not doing well Kirana Ghar, Mumbai Sastaa Bazaar, Lucknow Findings87654321 Research

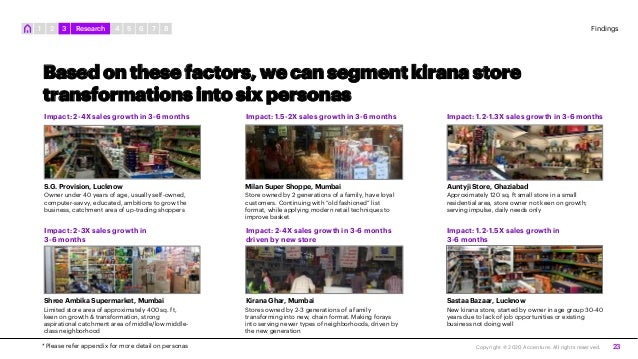

- 23. Copyright © 2020 Accenture. All rights reserved. 23 Based on these factors, we can segment kirana store transformations into six personas * Please refer appendix for more detail on personas Impact: 2-4X sales growth in 3-6 months Impact: 1.5-2X sales growth in 3-6 months Impact: 2-3X sales growth in 3-6 months Impact: 2-4X sales growth in 3-6 months driven by new store Impact: 1.2-1.5X sales growth in 3-6 months Findings Impact: 1.2-1.3X sales growth in 3-6 months 87654321 Research Owner under 40 years of age, usually self-owned, computer-savvy, educated, ambitions to grow the business, catchment area of up-trading shoppers Store owned by 2 generations of a family, have loyal customers. Continuing with “old fashioned” list format, while applying modern retail techniques to improve basket Approximately 120 sq. ft small store in a small residential area, store owner not keen on growth; serving impulse, daily needs only Limited store area of approximately 400 sq. ft, keen on growth & transformation, strong aspirational catchment area of middle/low middle- class neighborhood Stores owned by 2-3 generations of a family transforming into new, chain format. Making forays into serving newer types of neighborhoods, driven by the new generation New kirana store, started by owner in age group 30-40 years due to lack of job opportunities or existing business not doing well S.G. Provision, Lucknow Milan Super Shoppe, Mumbai Auntyji Store, Ghaziabad Shree Ambika Supermarket, Mumbai Kirana Ghar, Mumbai Sastaa Bazaar, Lucknow

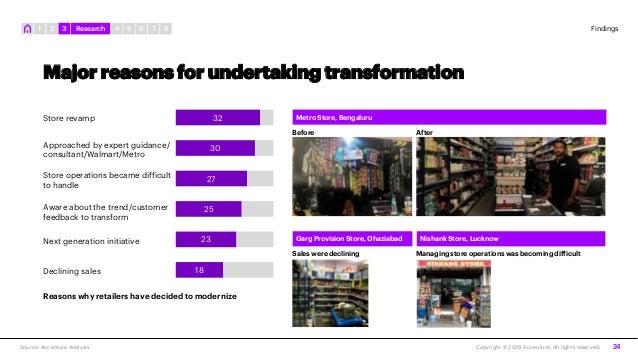

- 24. Copyright © 2020 Accenture. All rights reserved. 24 Major reasons for undertaking transformation Source: Accenture Analysis 32 30 27 25 23 18 Store revamp Approached by expert guidance/ consultant/Walmart/Metro Store operations became difficult to handle Aware about the trend/customer feedback to transform Next generation initiative Declining sales Reasons why retailers have decided to modernize Metro Store, Bengaluru Before After Garg Provision Store, Ghaziabad Nishank Store, Lucknow Sales were declining Managing store operations was becoming difficult Findings87654321 Research

- 25. Copyright © 2020 Accenture. All rights reserved. 25 Kirana transformation can also boost the rural consumption Source: Accenture Analysis 18 stores we spoke to, were present in small towns with population less than 1 lakh and the store owners are also interested in participating in the formal economy. • Even customers in small towns are aware about most of the brands (due to Internet and TV ads) and they want to buy them, but due to lack of supply, they need to go to nearby cities. • In many places, customers go to nearby large towns/districts/tehsil-level towns to buy their grocery. • Retailers are aware about the untapped consumption potential which small towns have. • Impact of modernization is on the higher side in such areas. Case Study – Saptashrungi Super Shoppee, Nandgaon, Maharashtra In this small town with less than 50,000 population, people used to go nearby cities like Malegaon and Nashik for their monthly grocery purchases and for a “mall experience.” The owner of this store saw a huge opportunity and transformed his store into a modern one. His stores sales have doubled today. Findings87654321 Research

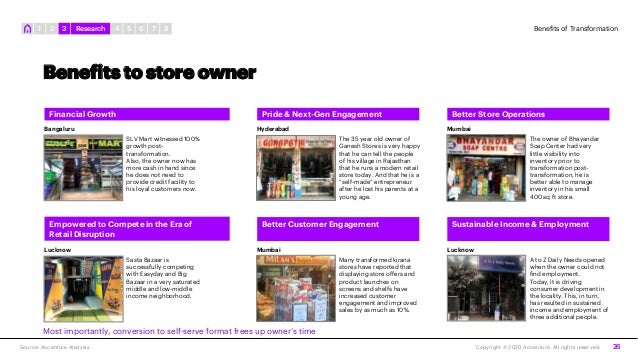

- 26. Copyright © 2020 Accenture. All rights reserved. 26 Benefits to store owner Source: Accenture Analysis Financial Growth Bangaluru SLV Mart witnessed 100% growth post- transformation. Also, the owner now has more cash in hand since he does not need to provide credit facility to his loyal customers now. Hyderabad The 35 year old owner of Ganesh Stores is very happy that he can tell the people of his village in Rajasthan that he runs a modern retail store today. And that he is a “self-made” entrepreneur after he lost his parents at a young age. Mumbai The owner of Bhayandar Soap Center had very little visibility into inventory prior to transformation post- transformation, he is better able to manage inventory in his small 400 sq ft store. Empowered to Compete in the Era of Retail Disruption Lucknow Sasta Bazaar is successfully competing with Easyday and Big Bazaar in a very saturated middle and low-middle income neighborhood. Better Customer Engagement Mumbai Many transformed kirana stores have reported that displaying store offers and product launches on screens and shelfs have increased customer engagement and improved sales by as much as 10%. Sustainable Income & Employment Lucknow A to Z Daily Needs opened when the owner could not find employment. Today, it is driving consumer development in the locality. This, in turn, has resulted in sustained income and employment of three additional people. Most importantly, conversion to self-serve format frees up owner’s time Benefits of Transformation Pride & Next-Gen Engagement Better Store Operations 87654321 Research

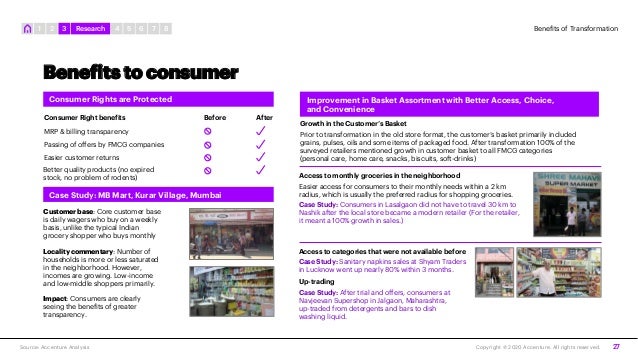

- 27. Copyright © 2020 Accenture. All rights reserved. 27 Benefits to consumer Source: Accenture Analysis MRP & billing transparency Passing of offers by FMCG companies Easier customer returns Better quality products (no expired stock, no problem of rodents) Consumer Right benefits Customer base: Core customer base is daily wagers who buy on a weekly basis, unlike the typical Indian grocery shopper who buys monthly Locality commentary: Number of households is more or less saturated in the neighborhood. However, incomes are growing. Low-income and low-middle shoppers primarily. Impact: Consumers are clearly seeing the benefits of greater transparency. Before After Case Study: MB Mart, Kurar Village, Mumbai Consumer Rights are Protected Improvement in Basket Assortment with Better Access, Choice, and Convenience Access to categories that were not available before Case Study: Sanitary napkins sales at Shyam Traders in Lucknow went up nearly 80% within 3 months. Growth in the Customer’s Basket Prior to transformation in the old store format, the customer’s basket primarily included grains, pulses, oils and some items of packaged food. After transformation 100% of the surveyed retailers mentioned growth in customer basket to all FMCG categories (personal care, home care, snacks, biscuits, soft-drinks) Up-trading Case Study: After trial and offers, consumers at Navjeevan Supershop in Jalgaon, Maharashtra, up-traded from detergents and bars to dish washing liquid. Access to monthly groceries in the neighborhood Easier access for consumers to their monthly needs within a 2 km radius, which is usually the preferred radius for shopping groceries. Case Study: Consumers in Lasalgaon did not have to travel 30 km to Nashik after the local store became a modern retailer (For the retailer, it meant a 100% growth in sales.) Benefits of Transformation87654321 Research

- 28. Copyright © 2020 Accenture. All rights reserved. 28 Benefits to government Source: Accenture Analysis Increase in Local Employment Formal Economy Increase in Tax Contribution • Transformation will promote both self-employment and employment of the local community. • Our research found an average 50% growth in employment post modernization. • Transformation of 1.4 M stores can generate 3.2 M NEW JOBS • Modernization of this industry can provide jobs to low-skilled people • Transformation of 1.4 M stores can provide could translate into a 250% growth in use of computerized billing and ledger system. Adoption of IT systems will enable the government to have better visibility and traceability into what was previously the "informal" economy. • Kirana transformation has led to an average 50% growth in tax contribution of retailers. • Transformation of 1.4 M stores can also boost income tax contribution from retail businesses by 240%, growth in income tax contribution from retail businesses, resulting in incremental income tax of approximately INR16 billion. Driving Rural Consumption • Modernization will drive consumption, including in under-served semi- urban and rural markets where current demands are unmet. • It will also help improve rural supply chain and accessibility. Positive Impact on Consumption & GDP Food Safety & Hygiene Boost for Domestic Industries • Modernization can provide a 5% to 20%* boost in consumption, which will positively impact GDP • Our research found about 50% store sales are now completed through non-cash payments. • Modernization will directly benefit the Digital India campaign. • Modernization will enable evolution of local players and supermarket chains across different cities / towns, which will naturally preserve local small-scale businesses such as food processing industries, home-made cuisines, etc. • Modernization will improve food safety and hygiene standards for the community. Benefits of Transformation87654321 Research

- 29. 29 TRANSFORMATION PROCESS

- 30. 30 SINCE ITWORKS, WHAT ARE THE STEPS IN KIRANA TRANSFORMATION? Copyright © 2020 Accenture. All rights reserved. 87654321 Transformation Process

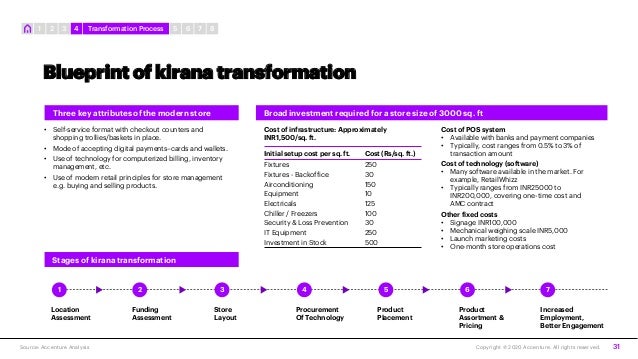

- 31. 31Copyright © 2020 Accenture. All rights reserved. Blueprint of kirana transformation Source: Accenture Analysis Three key attributes of the modern store Broad investment required for a store size of 3000 sq. ft • Self-service format with checkout counters and shopping trollies/baskets in place. • Mode of accepting digital payments–cards and wallets. • Use of technology for computerized billing, inventory management, etc. • Use of modern retail principles for store management e.g. buying and selling products. Initial setup cost per sq. ft. Cost (Rs/sq. ft.) Fixtures 250 Fixtures - Backoffice 30 Airconditioning 150 Equipment 10 Electricals 125 Chiller / Freezers 100 Security & Loss Prevention 30 IT Equipment 250 Investment in Stock 500 Cost of infrastructure: Approximately INR1,500/sq. ft. Cost of POS system • Available with banks and payment companies • Typically, cost ranges from 0.5% to 3% of transaction amount Cost of technology (software) • Many software available in the market. For example, RetailWhizz • Typically ranges from INR25000 to INR200,000, covering one-time cost and AMC contract Other fixed costs • Signage INR100,000 • Mechanical weighing scale INR5,000 • Launch marketing costs • One-month store operations cost Stages of kirana transformation Location Assessment Funding Assessment Store Layout Procurement Of Technology Product Placement Product Assortment & Pricing Increased Employment, Better Engagement 1 2 3 5 6 74 87654321 Transformation Process

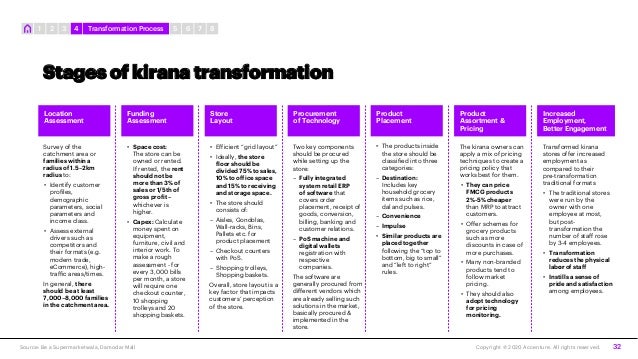

- 32. 32Copyright © 2020 Accenture. All rights reserved. Stages of kirana transformation Source: Be a Supermarketwala, Damodar Mall Location Assessment Funding Assessment Store Layout Procurement of Technology Product Placement Product Assortment & Pricing Increased Employment, Better Engagement Survey of the catchment area or families within a radius of 1.5–2km radius to: • Identify customer profiles, demographic parameters, social parameters and income class. • Assess external drivers such as competitors and their formats (e.g. modern trade, eCommerce), high- traffic areas/times. In general, there should be at least 7,000–8,000 families in the catchment area. • Space cost: The store can be owned or rented. If rented, the rent should not be more than 3% of sales or 1/5th of gross profit – whichever is higher. • Capex: Calculate money spent on equipment, furniture, civil and interior work. To make a rough assessment - for every 3,000 bills per month, a store will require one checkout counter, 10 shopping trolleys and 20 shopping baskets. • Efficient “grid layout” • Ideally, the store floor should be divided 75% to sales, 10% to office space and 15% to receiving and storage space. • The store should consists of: – Aisles, Gondolas, Wall-racks, Bins, Pallets etc. for product placement – Checkout counters with PoS. – Shopping trolleys, Shopping baskets. Overall, store layout is a key factor that impacts customers’ perception of the store. Two key components should be procured while setting up the store: – Fully integrated system retail ERP of software that covers order placement, receipt of goods, conversion, billing, banking and customer relations. – PoS machine and digital wallets registration with respective companies. The software are generally procured from different vendors which are already selling such solutions in the market, basically procured & implemented in the store. • The products inside the store should be classified into three categories: – Destination: Includes key household grocery items such as rice, dal and pulses. – Convenience – Impulse • Similar products are placed together following the “top to bottom, big to small” and “left to right” rules. The kirana owners can apply a mix of pricing techniques to create a pricing policy that works best for them. • They can price FMCG products 2%-5% cheaper than MRP to attract customers. • Offer schemes for grocery products such as more discounts in case of more purchases. • Many non-branded products tend to follow market pricing. • They should also adopt technology for pricing monitoring. Transformed kirana stores offer increased employment as compared to their pre-transformation traditional formats • The traditional stores were run by the owner with one employee at most, but post- transformation the number of staff rose by 3-4 employees. • Transformation reduces the physical labor of staff • Instills a sense of pride and satisfaction among employees. 87654321 Transformation Process

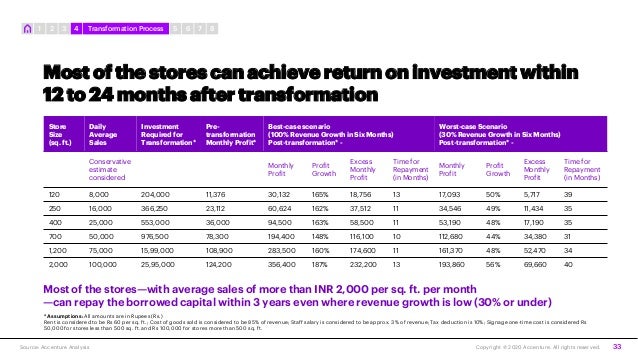

- 33. 33Copyright © 2020 Accenture. All rights reserved. Most of the stores can achieve return on investment within 12 to 24 months after transformation Source: Accenture Analysis Store Size (sq. ft.) Daily Average Sales Investment Required for Transformation* Pre- transformation Monthly Profit* Best-case scenario (100% Revenue Growth in Six Months) Post-transformation* - Worst-case Scenario (30% Revenue Growth in Six Months) Post-transformation* - Conservative estimate considered Monthly Profit Profit Growth Excess Monthly Profit Time for Repayment (in Months) Monthly Profit Profit Growth Excess Monthly Profit Time for Repayment (in Months) 120 8,000 204,000 11,376 30,132 165% 18,756 13 17,093 50% 5,717 39 250 16,000 366,250 23,112 60,624 162% 37,512 11 34,546 49% 11,434 35 400 25,000 553,000 36,000 94,500 163% 58,500 11 53,190 48% 17,190 35 700 50,000 976,500 78,300 194,400 148% 116,100 10 112,680 44% 34,380 31 1,200 75,000 15,99,000 108,900 283,500 160% 174,600 11 161,370 48% 52,470 34 2,000 100,000 25,95,000 124,200 356,400 187% 232,200 13 193,860 56% 69,660 40 * Assumptions: All amounts are in Rupees (Rs.) Rent is considered to be Rs 60 per sq. ft.; Cost of goods sold is considered to be 85% of revenue; Staff salary is considered to be approx. 3% of revenue; Tax deduction is 10%; Signage one-time cost is considered Rs 50,000 for stores less than 500 sq. ft. and Rs 100,000 for stores more than 500 sq. ft. Most of the stores—with average sales of more than INR 2,000 per sq. ft. per month —can repay the borrowed capital within 3 years even where revenue growth is low (30% or under) 87654321 Transformation Process

- 34. 34 CHALLENGES

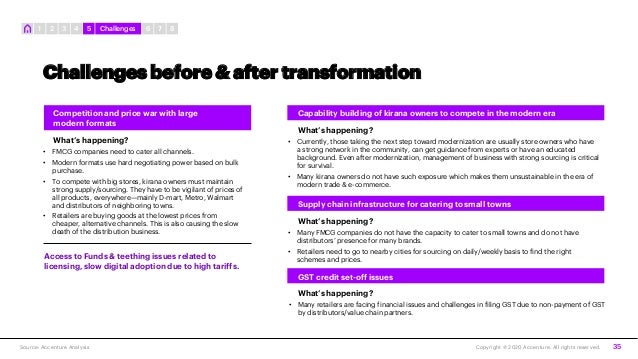

- 35. 35Copyright © 2020 Accenture. All rights reserved. Challenges before & after transformation Source: Accenture Analysis Competition and price war with large modern formats What’s happening? • FMCG companies need to cater all channels. • Modern formats use hard negotiating power based on bulk purchase. • To compete with big stores, kirana owners must maintain strong supply/sourcing. They have to be vigilant of prices of all products, everywhere—mainly D-mart, Metro, Walmart and distributors of neighboring towns. • Retailers are buying goods at the lowest prices from cheaper, alternative channels. This is also causing the slow death of the distribution business. Access to Funds & teething issues related to licensing, slow digital adoption due to high tariffs. Capability building of kirana owners to compete in the modern era What’s happening? • Currently, those taking the next step toward modernization are usually store owners who have a strong network in the community, can get guidance from experts or have an educated background. Even after modernization, management of business with strong sourcing is critical for survival. • Many kirana owners do not have such exposure which makes them unsustainable in the era of modern trade & e-commerce. Supply chain infrastructure for catering to small towns What’s happening? • Many FMCG companies do not have the capacity to cater to small towns and do not have distributors’ presence for many brands. • Retailers need to go to nearby cities for sourcing on daily/weekly basis to find the right schemes and prices. GST credit set-off issues What’s happening? • Many retailers are facing financial issues and challenges in filing GST due to non-payment of GST by distributors/value chain partners. 87654321 Challenges

- 36. 36Copyright © 2020 Accenture. All rights reserved. Even large independent modern chains are finding it difficult to sustain operations Source: Accenture Analysis Large supermarket chain in Hyderabad Many retailers think growth in the business will improve their quality of life, however this growth also comes with increased costs and multiple difficulties in managing the business. One of the popular chains in Hyderabad, this supermarket is still finding it extremely hard to survive in near future due to tremendous competition with large modern formats, increasing real estate costs to sustain brick-and-mortar business and increased overhead costs of modern retail. 87654321 Challenges

- 37. 37 ROLE OF STAKEHOLDERS

- 38. SO, WHAT ARETHEENABLERS FOR KIRANA STORE OWNERS TO OVERCOME THESE CHALLENGES? Copyright © 2020 Accenture. All rights reserved. 38 STAKEHOLDERS 87654321 Role of Stakeholders

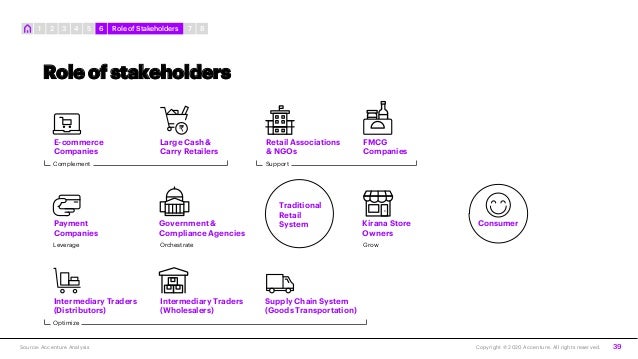

- 39. Intermediary Traders (Wholesalers) Supply Chain System (Goods Transportation) Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 39 Role of stakeholders Payment Companies Traditional Retail System E-commerce Companies Large Cash & Carry Retailers Complement Retail Associations & NGOs FMCG Companies Support Leverage Government & Compliance Agencies Orchestrate Kirana Store Owners Grow Intermediary Traders (Distributors) Optimize Consumer 87654321 Role of Stakeholders

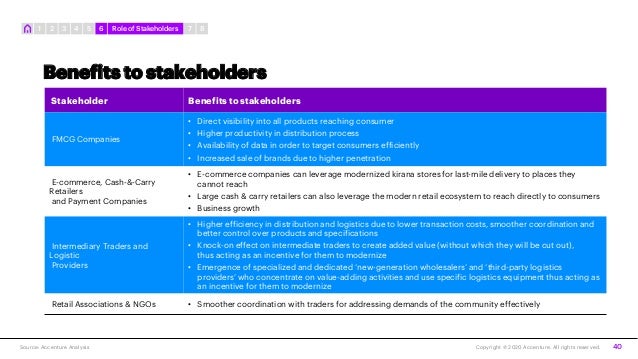

- 40. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 40 Benefits to stakeholders Stakeholder Benefits to stakeholders FMCG Companies • Direct visibility into all products reaching consumer • Higher productivity in distribution process • Availability of data in order to target consumers efficiently • Increased sale of brands due to higher penetration E-commerce, Cash-&-Carry Retailers and Payment Companies • E-commerce companies can leverage modernized kirana stores for last-mile delivery to places they cannot reach • Large cash & carry retailers can also leverage the modern retail ecosystem to reach directly to consumers • Business growth Intermediary Traders and Logistic Providers • Higher efficiency in distribution and logistics due to lower transaction costs, smoother coordination and better control over products and specifications • Knock-on effect on intermediate traders to create added value (without which they will be cut out), thus acting as an incentive for them to modernize • Emergence of specialized and dedicated ‘new-generation wholesalers’ and ‘third-party logistics providers’ who concentrate on value-adding activities and use specific logistics equipment thus acting as an incentive for them to modernize Retail Associations & NGOs • Smoother coordination with traders for addressing demands of the community effectively 87654321 Role of Stakeholders

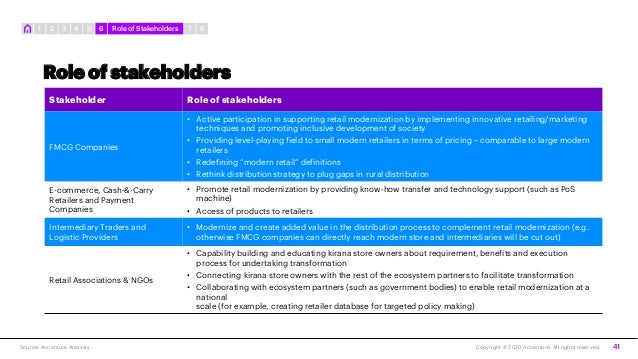

- 41. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 41 Role of stakeholders Stakeholder Role of stakeholders FMCG Companies • Active participation in supporting retail modernization by implementing innovative retailing/marketing techniques and promoting inclusive development of society • Providing level-playing field to small modern retailers in terms of pricing – comparable to large modern retailers • Redefining “modern retail” definitions • Rethink distribution strategy to plug gaps in rural distribution E-commerce, Cash-&-Carry Retailers and Payment Companies • Promote retail modernization by providing know-how transfer and technology support (such as PoS machine) • Access of products to retailers Intermediary Traders and Logistic Providers • Modernize and create added value in the distribution process to complement retail modernization (e.g. otherwise FMCG companies can directly reach modern store and intermediaries will be cut out) Retail Associations & NGOs • Capability building and educating kirana store owners about requirement, benefits and execution process for undertaking transformation • Connecting kirana store owners with the rest of the ecosystem partners to facilitate transformation • Collaborating with ecosystem partners (such as government bodies) to enable retail modernization at a national scale (for example, creating retailer database for targeted policy making) 87654321 Role of Stakeholders

- 42. 42 RECOMMENDATIONS

- 43. WHAT SHOULD BEDONETO EXPEDITE RETAIL MODERNIZATION IN ASUSTAINABLE MANNER? ROLE OFGOVERNMENT AND RECOMMENDATIONS Copyright © 2020 Accenture. All rights reserved. 43 87654321 Recommendations

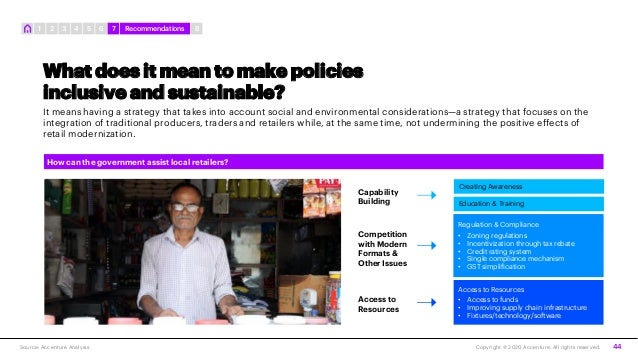

- 44. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 44 What does it mean to make policies inclusive and sustainable? It means having a strategy that takes into account social and environmental considerations—a strategy that focuses on the integration of traditional producers, traders and retailers while, at the same time, not undermining the positive effects of retail modernization. Regulation & Compliance • Zoning regulations • Incentivization through tax rebate • Credit rating system • Single compliance mechanism • GST simplification Access to Resources • Access to funds • Improving supply chain infrastructure • Fixtures/technology/software Education & Training Creating Awareness How can the government assist local retailers? Capability Building Competition with Modern Formats & Other Issues Access to Resources 87654321 Recommendations

- 45. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 45 • We think the government is best placed to launch awareness campaigns on kirana store transformation through newspaper and other key media channels. • The key aspects for communication include why and how kiranas should modernize and what is in it for them. 01 Create awareness through media campaigns Creating Awareness87654321 Recommendations

- 46. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 46 Undertaking large-scale programs for capability building for kirana store owners/managers: • through ITI. • organizing locality-wise independent sessions by experts. For example, the Chinese government offered improved infrastructure for relocated retailers and trained them in business skills and food safety. The result: goods offered for sale in the wet markets became safer and more hygienic. Tax payments also increased. 02 Undertaking large-scale programs for capability building Education & Training87654321 Recommendations

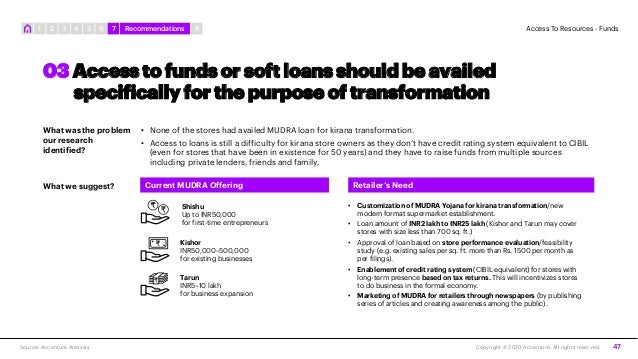

- 47. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 47 • None of the stores had availed MUDRA loan for kirana transformation. • Access to loans is still a difficulty for kirana store owners as they don’t have credit rating system equivalent to CIBIL (even for stores that have been in existence for 50 years) and they have to raise funds from multiple sources including private lenders, friends and family. 03 Access to funds or soft loans should be availed specifically for the purpose of transformation What was the problem our research identified? • Customization of MUDRA Yojana for kirana transformation/new modern format supermarket establishment. • Loan amount of INR2 lakh to INR25 lakh (Kishor and Tarun may cover stores with size less than 700 sq. ft.) • Approval of loan based on store performance evaluation/feasibility study (e.g. existing sales per sq. ft. more than Rs. 1500 per month as per filings). • Enablement of credit rating system (CIBIL equivalent) for stores with long-term presence based on tax returns. This will incentivizes stores to do business in the formal economy. • Marketing of MUDRA for retailers through newspapers (by publishing series of articles and creating awareness among the public). Current MUDRA Offering Retailer’s Need Shishu Up to INR50,000 for first-time entrepreneurs Kishor INR50,000–500,000 for existing businesses Tarun INR5–10 lakh for business expansion What we suggest? Access To Resources - Funds87654321 Recommendations

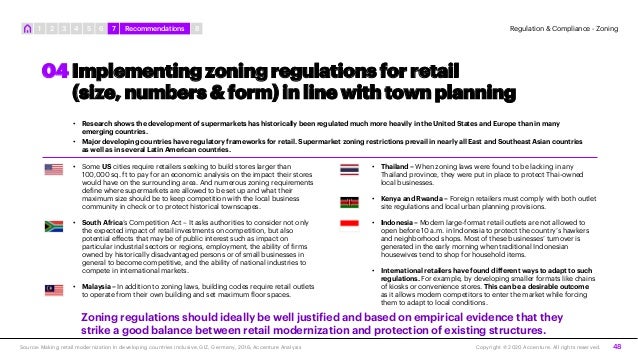

- 48. Copyright © 2020 Accenture. All rights reserved.Source: Making retail modernization In developing countries inclusive, GIZ, Germany, 2016; Accenture Analysis 48 • Research shows the development of supermarkets has historically been regulated much more heavily in the United States and Europe than in many emerging countries. • Major developing countries have regulatory frameworks for retail. Supermarket zoning restrictions prevail in nearly all East and Southeast Asian countries as well as in several Latin American countries. 04 Implementing zoning regulations for retail (size, numbers & form) in line with town planning • Some US cities require retailers seeking to build stores larger than 100,000 sq. ft to pay for an economic analysis on the impact their stores would have on the surrounding area. And numerous zoning requirements define where supermarkets are allowed to be set up and what their maximum size should be to keep competition with the local business community in check or to protect historical townscapes. • South Africa’s Competition Act – It asks authorities to consider not only the expected impact of retail investments on competition, but also potential effects that may be of public interest such as impact on particular industrial sectors or regions, employment, the ability of firms owned by historically disadvantaged persons or of small businesses in general to become competitive, and the ability of national industries to compete in international markets. • Malaysia – In addition to zoning laws, building codes require retail outlets to operate from their own building and set maximum floor spaces. • Thailand – When zoning laws were found to be lacking in any Thailand province, they were put in place to protect Thai-owned local businesses. • Kenya and Rwanda – Foreign retailers must comply with both outlet site regulations and local urban planning provisions. • Indonesia – Modern large-format retail outlets are not allowed to open before 10 a.m. in Indonesia to protect the country’s hawkers and neighborhood shops. Most of these businesses’ turnover is generated in the early morning when traditional Indonesian housewives tend to shop for household items. • International retailers have found different ways to adapt to such regulations. For example, by developing smaller formats like chains of kiosks or convenience stores. This can be a desirable outcome as it allows modern competitors to enter the market while forcing them to adapt to local conditions. Zoning regulations should ideally be well justified and based on empirical evidence that they strike a good balance between retail modernization and protection of existing structures. Regulation & Compliance - Zoning87654321 Recommendations

- 49. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 49 • Enablement of credit rating system based on income tax filings incentivizes store owner to do business in the formal economy as this credit rating will enable their access to funds. • Also, incentivization in the form of tax rebate for transformed stores can be given in order to promote modernization (based on limits on number, size and form of the store). 05 Incentivization for doing business in the formal economy Regulation & Compliance87654321 Recommendations

- 50. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 50 Single licensing mechanism can be introduced for opening supermarkets. This can: • Reduce the cost of compliance. • Simplify the process for retailers. • Promote ease of doing business in the country. 06 Single licensing mechanism Regulation & Compliance87654321 Recommendations

- 51. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 51 • In many areas, retailers are facing credit set-off issues due to delayed submission by value chain partner. • Delayed GST submissions by suppliers' blocks retailer's money, hampering his working capital • Hence, simplifying GST filing and collection process is necessary to overcome teething trade issues being faced by retailers 07 GST simplification to mitigate credit set-off issue Regulation & Compliance87654321 Recommendations

- 52. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 52 • Improving rural supply chain in remote areas in order to make goods and supplies accessible. • Upgradation and facilitation of infrastructure for retail and logistic zones (China, for instance, developed its markets using public-private partnership and privatizing management). 08 Improving supply chain infrastructure Access To Resources87654321 Recommendations

- 53. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 53 • Access to cheaper resources required for transformation. • Subsidizing technology cost – assistance to adopt digital payment systems. • Availability of centralized umbrella software for governing grocery retail (similar to the concept of Unified Payments Interface). 09 Easier and cheaper access to technology and fixtures Access To Resources87654321 Recommendations

- 54. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 54 • The government can influence companies to participate in kirana transformation as part of their CSR activities • Top 100 listed companies in India spent nearly US$1 billion on CSR activities in FY18, up 47% than in 2014* 10 Influence private sector to assist in kirana store modernization Access To Resources * Note: 2014 was the year when Government of India made it mandatory for large companies to participate on special development projects, with an investment of 2% of their net profits 87654321 Recommendations

- 55. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 55 • We recommend undertaking a pilot of kirana transformation pilot in one state first. • This will be an 8-12 month project to modernize x% kirana stores in that state. • Findings from the pilot can later be applied for a large-scale rollout across the rest of the country. • Key drivers which will influence which state to consider are: How? Pilot for kirana transformation 87654321 Recommendations • Consumer readiness • Kirana store owners’ readiness • Presence of key ecosystem partners to aid in modernization. For example, FMCG companies and associations. • State government/organization support.

- 56. Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 56 What TRRAIN is doing? Motivating Kirana Store Owners Education & Know-How Transfer Ecosystem Engagement Rewards & Recognitions Series of YouTube videos explaining the importance and execution of kirana transformation and all aspects of the management of the business • Seminars • Success Stories Case Study • Contact Programs • Awareness through Social Media & Websites • One-day Basic Course • 3 Days’ Advance Course • Comprehensive Certificate Course • Diploma Course • Consultants • Fixture Suppliers • System Suppliers • Other Vendors to Support Transformation Projects 200+Kirana transformations done along with multiple partners 87654321 Recommendations

- 57. 57 APPENDIX

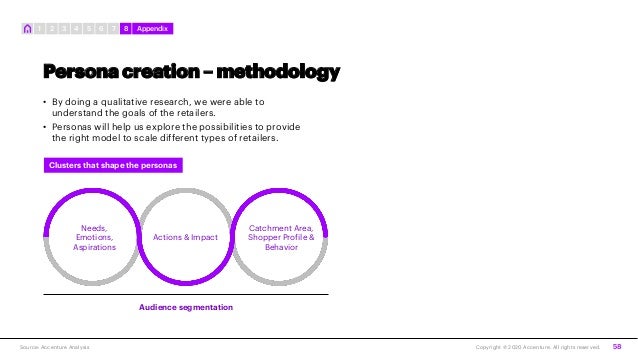

- 58. Persona creation – methodology • By doing a qualitative research, we were able to understand the goals of the retailers. • Personas will help us explore the possibilities to provide the right model to scale different types of retailers. Clusters that shape the personas Copyright © 2020 Accenture. All rights reserved.Source: Accenture Analysis 58 Needs, Emotions, Aspirations Actions & Impact Catchment Area, Shopper Profile & Behavior Audience segmentation 87654321 Appendix

- 59. 59 Young owner (under 40 years of age), usually self-owned, computer/Internet-savvy, educated, ambitions to grow the business, catchment area of up-trading shoppers mostly under-served by big retail stores.(For instance, Saurabh) Uptrading mid/low income consumers. Currently not very used to shopping in supermarkets. But starting to enjoy the shopping experiences they provide. Highly value conscious. But open to trying particularly new brands of food/beverages. Highly aspirational. Retail/kirana formats still under-developed in the neighborhood. Both “list based” buyers plus growing walk-in, impulse purchasers Highly positive – welcomes external help in transformation. Usually, these transformations are self-started by ambitious owners. They then employ family members to manage growing operations or employ new people (1-3 new members). Very open to receiving and applying store training, aid and software from experienced partners. Willing to invest up to INR2 lakh in it. Easy adoption of software (and CCTV) to manage store ops. Actively churn inventory, storage far lower – on a weekly, fortnightly basis. Observe shoppers keenly and rotate/order new SKUs such as peanut butter and brown bread based on customer demand. Many of them prefer digital orders to FMCG companies versus physical orders because of lead time. Impact 2-4X improvement in sales observed in the 3-6 month period after transformation. Persona 187654321 Appendix Shoppers profile Attitude and drive toward transformation Post-transformation adoption of modern retail techniques

- 60. 60 Store has been with one family for 2-3 generations, have loyal old customers and happily serve them by retaining the “old fashioned” kirana format, while applying modern retail techniques to manage store operations and improve basket size/assortment (For instance, Milan Supermarket) Usually high and middle-income consumers. Have a large shopping list on a monthly basis (INR10,000+ per household). Apart from a fixed list, likes to be able to see/pick and choose among the brands visible in the shelf. Value conscious – but could potentially up-trade to try particularly new brands of impulse food and beverages. Values the familiar/accessible neighborhood store owner who could even potentially do home delivery/send someone along to drop groceries Usually second or third-generation owners could be open to transformation, particularly the self-serve aspect of an ‘old store’. But some members, including those from the older generation, have reservations about change in assortment, use of software (which may make their earnings transparent, hence bring tax accountability). But usually have larger spaces to transform (500+ sq. ft.). Overall mixed attitude, especially from those who still have not seen the benefits of transformation. Mixed adoption of software (and CCTV) to manage store ops. Inventory churn better – target 30-45 days. Earlier, it used to be 45-60 days, with a high 20-30% of expired/unused stock. Always been a keen observer of shopper behavior and demand – and continue to do so. Software is an additional aid for those who adopted it. FMCG companies starting to consider them as supermarkets given their size/turnover/ability for display, etc. Impact Atleast 1.5-2X improvement in sales observed in the 3-6 month period after transformation. Increase in employment: At least 40%. Persona 287654321 Appendix Shoppers profile Attitude and drive toward transformation Post-transformation adoption of modern retail techniques

- 61. 61 Very small store of less than 160 sq. ft, limited residential area, store owner not keen on growth, serving impulse, daily needs only primarily snacks, biscuits, ice-creams, beverages, small pack skin and home care items, small quantities of pulses, oils, etc. (For instance, Auntyji Store) Usually middle-income neighborhood. Displays highly value-seeking behavior. Time is not a huge constraint. Would rather buy monthly groceries in a modern retail format or from eCommerce sites wherever it is cheaper. Neighborhood is highly residential, society with limited scope for growth. Shopping seen as an excursion like going to malls on a weekly basis. Moved away from buying from kiranas to malls over the years. The neighbourhood kirana store is only to fulfill replenishment items/impulse buys. Typically, these are 120-160 sq. ft. stores. Attitude to transformation still not clear as not many of the shops of this size have not found a clear model of transformation for such a small format. The stores we visited were newly opened with owners having low experience in running a kirana business. So, they were happy to receive external help. They also like that storage is better–inventory churned faster after transformation. Low adoption of software/CCTV as everything can be “seen.” Inventory churn better – target 7-21 days. Earlier, it used to be 1 month with lesser visibility of what was available/expired/moving. Better assortment management as there is limited shelf space. Storekeeper still the primary means to observe and react to shopper demand. Not much attention received from FMCG companies. Shoppers profile Attitude and drive toward transformation Post-transformation adoption of modern retail techniques Impact 20-30% increase in the 3-4 month period after transformation. No change in employment. More of a self-employment/survival model (needs to be tested further). Persona 387654321 Appendix

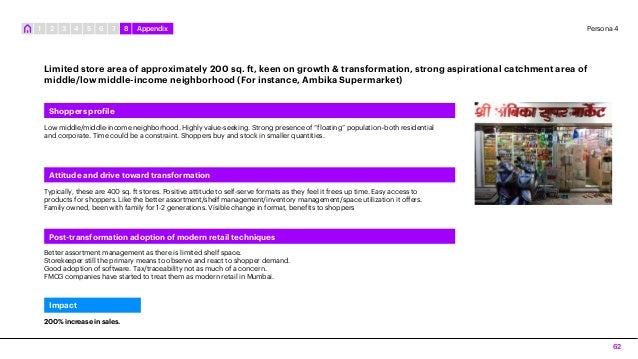

- 62. 62 Limited store area of approximately 200 sq. ft, keen on growth & transformation, strong aspirational catchment area of middle/low middle-income neighborhood (For instance, Ambika Supermarket) Low middle/middle-income neighborhood. Highly value-seeking. Strong presence of “floating” population–both residential and corporate. Time could be a constraint. Shoppers buy and stock in smaller quantities. Typically, these are 400 sq. ft stores. Positive attitude to self-serve formats as they feel it frees up time. Easy access to products for shoppers. Like the better assortment/shelf management/inventory management/space utilization it offers. Family owned, been with family for 1-2 generations. Visible change in format, benefits to shoppers Better assortment management as there is limited shelf space. Storekeeper still the primary means to observe and react to shopper demand. Good adoption of software. Tax/traceability not as much of a concern. FMCG companies have started to treat them as modern retail in Mumbai. Impact 200% increase in sales. Persona 487654321 Appendix Shoppers profile Attitude and drive toward transformation Post-transformation adoption of modern retail techniques

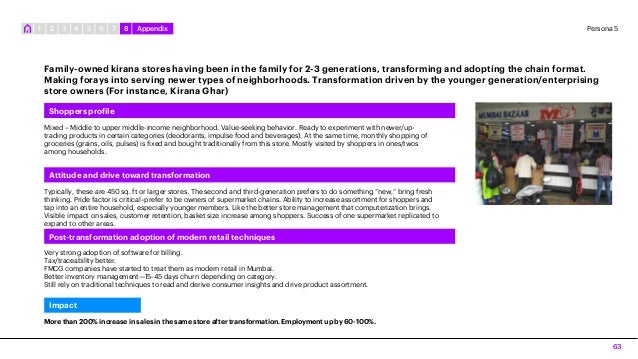

- 63. 63 Family-owned kirana stores having been in the family for 2-3 generations, transforming and adopting the chain format. Making forays into serving newer types of neighborhoods. Transformation driven by the younger generation/enterprising store owners (For instance, Kirana Ghar) Mixed – Middle to upper middle-income neighborhood. Value-seeking behavior. Ready to experiment with newer/up- trading products in certain categories (deodorants, impulse food and beverages). At the same time, monthly shopping of groceries (grains, oils, pulses) is fixed and bought traditionally from this store. Mostly visited by shoppers in ones/twos among households. Typically, these are 450 sq. ft or larger stores. The second and third-generation prefers to do something “new,” bring fresh thinking. Pride factor is critical–prefer to be owners of supermarket chains. Ability to increase assortment for shoppers and tap into an entire household, especially younger members. Like the better store management that computerization brings. Visible impact on sales, customer retention, basket size increase among shoppers. Success of one supermarket replicated to expand to other areas. Very strong adoption of software for billing. Tax/traceability better. FMCG companies have started to treat them as modern retail in Mumbai. Better inventory management—15-45 days churn depending on category. Still rely on traditional techniques to read and derive consumer insights and drive product assortment. Impact More than 200% increase in sales in the same store after transformation. Employment up by 60-100%. Persona 587654321 Appendix Shoppers profile Attitude and drive toward transformation Post-transformation adoption of modern retail techniques

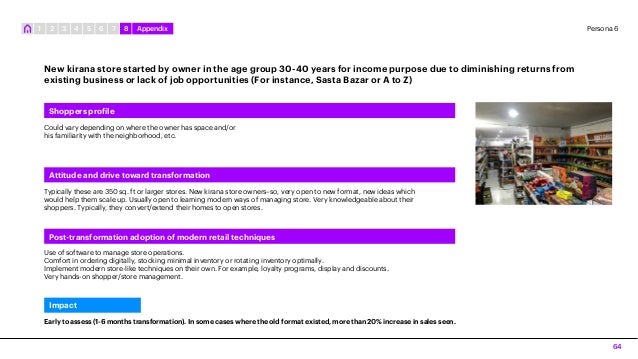

- 64. 64 New kirana store started by owner in the age group 30-40 years for income purpose due to diminishing returns from existing business or lack of job opportunities (For instance, Sasta Bazar or A to Z) Could vary depending on where the owner has space and/or his familiarity with the neighborhood, etc. Typically these are 350 sq. ft or larger stores. New kirana store owners–so, very open to new format, new ideas which would help them scale up. Usually open to learning modern ways of managing store. Very knowledgeable about their shoppers. Typically, they convert/extend their homes to open stores. Use of software to manage store operations. Comfort in ordering digitally, stocking minimal inventory or rotating inventory optimally. Implement modern store-like techniques on their own. For example, loyalty programs, display and discounts. Very hands-on shopper/store management. Impact Early to assess (1-6 months transformation). In some cases where the old format existed, more than 20% increase in sales seen. Persona 687654321 Appendix Shoppers profile Attitude and drive toward transformation Post-transformation adoption of modern retail techniques

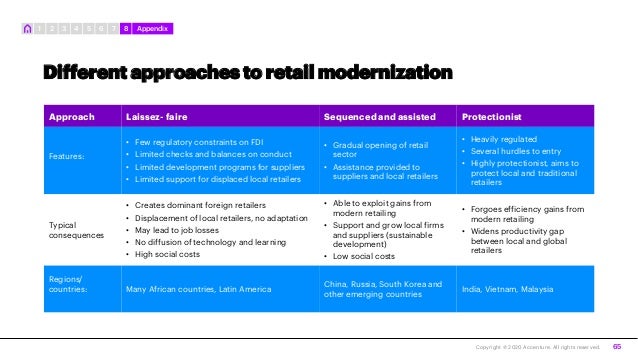

- 65. 65 Different approaches to retail modernization Approach Laissez- faire Sequenced and assisted Protectionist Features: • Few regulatory constraints on FDI • Limited checks and balances on conduct • Limited development programs for suppliers • Limited support for displaced local retailers • Gradual opening of retail sector • Assistance provided to suppliers and local retailers • Heavily regulated • Several hurdles to entry • Highly protectionist, aims to protect local and traditional retailers Typical consequences • Creates dominant foreign retailers • Displacement of local retailers, no adaptation • May lead to job losses • No diffusion of technology and learning • High social costs • Able to exploit gains from modern retailing • Support and grow local firms and suppliers (sustainable development) • Low social costs • Forgoes efficiency gains from modern retailing • Widens productivity gap between local and global retailers Regions/ countries: Many African countries, Latin America China, Russia, South Korea and other emerging countries India, Vietnam, Malaysia Copyright © 2020 Accenture. All rights reserved. 87654321 Appendix

- 66. 66 Factors driving impact of transformation Copyright © 2020 Accenture. All rights reserved. Potential of the locality Optimistic Scenario Pessimistic Scenario Areas with highly untapped consumption potential. For instance, outskirts of city, sub-urban areas, high footfall areas like market or railway station. Stores may acquire new customers in such areas. Very limited scope to extend the basket size of existing customers. For example, store within a society. Guidance received from experts in the field with regular monitoring Complete renovation or new setup with large investment, change of location Guidance received from entity with very low involvement in store business and low involvement by owner Only change of shelf and store layout. This may result in increased consumption by existing customers (due to increased visibility of products, large packs) In such cases, sales growth of 100–300% can be observed. In such cases, sales growth of 20–50% can be observed. Guidance received and owner’s DNA Level of transformation completed 01 02 03 87654321 Appendix

- 67. 67Copyright © 2020 Accenture. All rights reserved. Emerging economies have also used zoning laws to regulate wet markets China upgraded and trained business skills and food safety measures for wet markets and street hawkers • Governments in emerging and developing economies have traditionally used zoning laws to regulate wet markets and street hawkers in city centers—not just to prevent street congestion, but also because informal retail activities are difficult to tax and wet markets in particular often cause hygiene problems. Many governments, therefore, impose strict zoning regulations and hygiene standards for wet markets. An example is China. When implementing these instruments, China, for instance, also included major upgrading and development measures for street hawkers. Rather than leave wet markets to flounder and collapse, the Chinese approach was based on “retaining but modernizing.” This included experimenting with the privatization of wet market management, relocating hawkers and wet markets to uncongested and permanent sites, and training hawkers in business skills and food safety. The result? Goods on sale in the wet markets became safer and more hygienic. Tax payments also increased. • In case of India, there is no exclusive regulatory framework for the retail sector. Regulation of the retail sector is mainly in the domain of state governments. Different state governments have used different regulations to protect small unorganized retailers from retail giants. 87654321 Appendix

- 68. THANK YOU

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

반응형

'정보공유' 카테고리의 다른 글

| 경기도 재난지원금 (0) | 2021.08.14 |

|---|---|

| [NDC17] 왓 스튜디오 서비스파트 (1) | 2020.11.11 |

| NDC 2017 마이크로토크 - 프로그래머가 뉴스 읽는 법 (0) | 2020.11.11 |

| Digital 2020 Global Digital Overview (January 2020) v01 (0) | 2020.11.07 |

| Kirana Transformation in India (0) | 2020.11.07 |

| Impact of COVID-19: Tune In To Student Sentiments (0) | 2020.11.07 |